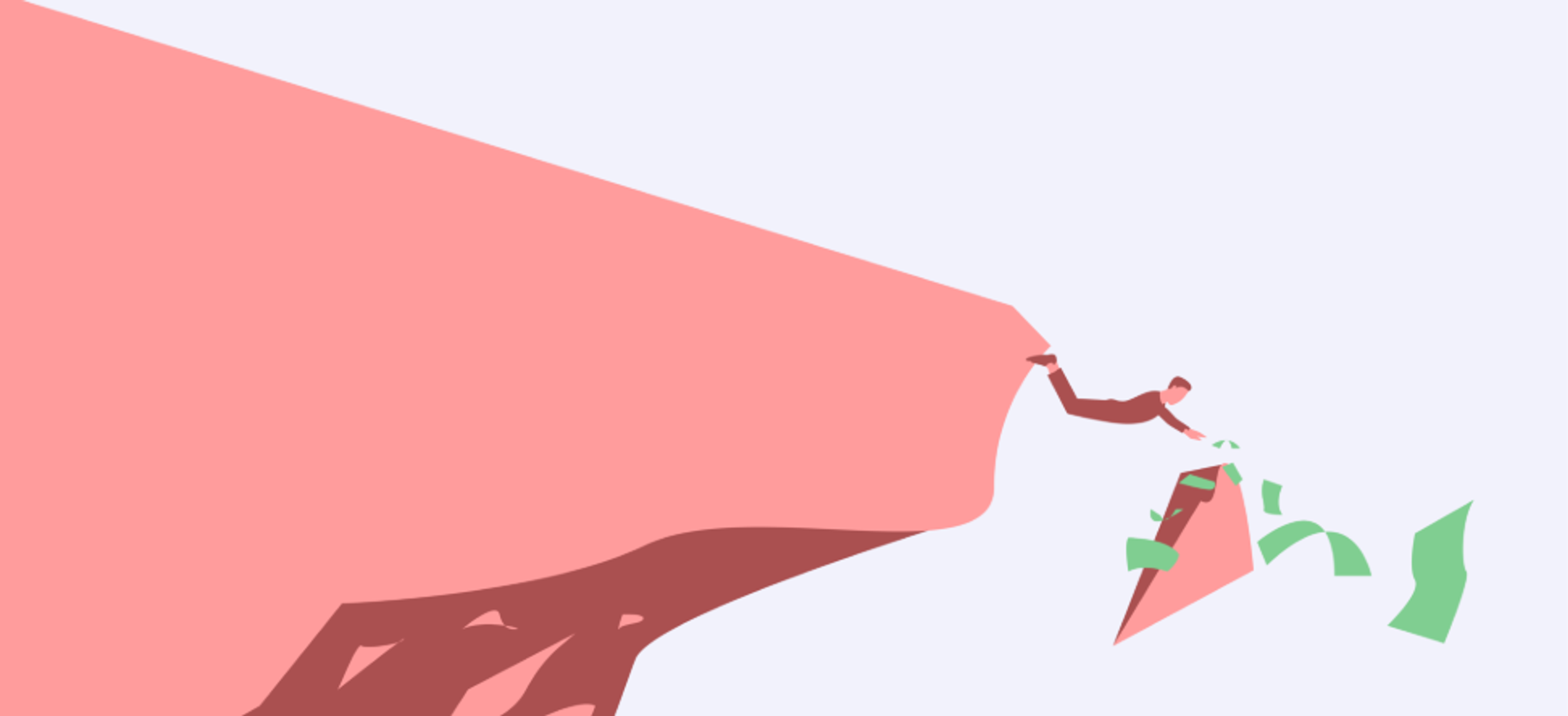

How the “benefits cliff” traps people in poverty

Image by Jihoo Yang

Jack Walker

- Street paper news

The article below was originally published by Street Sense Media.

Imagine two single parents raising toddlers in DC. One has an annual salary of $65,000, while the other earns $11,000 a year by working part-time. Their financial situations seem quite different; the parent paid more has much more money at their disposal, right?

Financial analysts say not necessarily. These Washingtonians likely have similar amounts to spend each month, and not because one uses their dollars more judiciously. Experts chalk it up to a phenomenon known as the “benefits cliff.”

In the US, many public assistance resources – like Medicaid and the Supplemental Nutrition Assistance Program (SNAP) – are based on income. For people with the greatest financial need, public benefits programs make it possible to pay grocery bills, childcare costs, and even rent.

Generally speaking, the less someone earns, the more resources they receive. But these programs also come with income restrictions, which cut residents off from benefits as their salaries rise. For a person earning $65,000 a year, this gap in coverage can stall their spending power at nearly one-eighth of their actual salary, making the road to higher earnings rocky.

A sudden drop-off

Rachelle Ellison is a Street Sense Media vendor – and the assistant director of a local housing advocacy group called the People for Fairness Coalition. Her work today is informed by the 17 years she spent navigating homelessness herself, all while struggling with co-occurring health issues like lupus, coronary artery disease, and emphysema.

A certified peer specialist and substance use disorder recovery coach, Ellison says that her path to long-term employment has been riddled with obstacles. In 2019, she finally found a full-time job that fit her needs and passions, working as a case manager for a local substance use disorder treatment center.

“I loved that job,” she says. “It was so amazing.”

Then, she learned that her Medicaid benefits were about to be terminated. The salary increase from her new job pushed her above the threshold for program eligibility, which left her with a tough choice. If she took the new, higher-paying job, she would have to swap healthcare plans and forego months of coverage in the process.

Given her medical history, that felt like too much of a risk. She decided to leave the new role.

“Even though these organizations that I work for have great benefits, you have to work 90 days before they take effect,” she says. “I had no insurance coverage. If anything would have happened, I would have been in debt. I had to resign.”

Ellison is not alone. Across the District, low-income residents seeking long-term employment face uncertainty and difficult decisions as they lose access to public benefits.

D.C. has one of the most robust social safety nets in the US. Take, for example, Temporary Assistance for Needy Families (TANF), a federally funded cash payment program. As of 2022, a DC family of three could receive as much as $665 per month in TANF funding, more than they could get in 40 other US states.

But benefits like TANF, SNAP, and the city’s Childcare and Development Fund (CCDF) subsidies are income dependent, which means that an increase in household income can be countered with a loss in public assistance. Residents must pay more to cover their needs, which means that raises in pay do not always translate to increases in quality of living, or the ability to save up for big purchases.

Plus, living in the District is expensive. This year, the Council for Community and Economic Research found that DC has the ninth-highest cost of living out of any city in the nation.

Employers in urban areas tend to pay their workers more, which can offset some of the costs associated with city life. But that higher salary can disqualify households from benefits programs administered by the federal government, which might set participation guidelines based on lower national averages for pay.

For example, while TANF eligibility guidelines vary by state, SNAP eligibility is based on the federal poverty line. Households experiencing financial insecurity by local standards might be overlooked by aid from the national level.

“What ends up happening is that individuals who are on public assistance, because they are making more in a high-cost metro, are closer to income thresholds that will kick them off of public assistance programs,” says Alvaro Sanchez, a senior research analyst with the Federal Reserve Bank of Atlanta. “That can pose a pretty serious challenge for people in places like DC.”

Sanchez co-authored a September 2023 paper on the benefits cliff and workforce development efforts in the District. He says that a gradual loss in public assistance can jeopardize a low or middle-income household’s long-term financial stability.

In Ellison’s case, an increase in income meant suddenly becoming ineligible for her healthcare plan, a problem that she encountered more than once.

After leaving her job as a case manager, she eventually found another full-time role as a recovery coach at Howard University Hospital. Like clockwork, she was notified that the added pay meant that she would lose Medicaid. She chose to depart from that position, too.

Since then, Ellison has settled for part-time and contract work that provides consistent pay but doesn’t jeopardize health insurance. While she wants the benefits and responsibility of a full-time position, she says that the transition period is just too big a risk.

“Every area that I have been able to overcome barriers, I wanted to get credentialed. I already have the lived expertise to help other people,” she says. “But with these income benefit cliffs, it’s another barrier put in our way.”

Seeking local solutions

Meanwhile, DC benefits administrators say that they are aware that the benefits cliff exists and are launching specific programming to address it.

“Most of our benefits that families and individuals [that are low income] in the District receive are federally supported, and have really strict rules,” says Geoff King of the DC Department of Human Services (DHS). This means that, for households, the benefits cliff can pose a “penalty for doing what they need to do to advance and earn more.”

In December 2022, DHS launched a program called the DC Career Mobility Action Plan, or Career MAP. King serves as program manager and says that Career MAP aims to alleviate the burden on families as they transition out of public assistance programs.

Career MAP provides support to offset decreasing benefits through a “combination” of means, ranging from rent discounts to annual cash payments of up to $10,000 per year, King says. This ensures that participants are “keeping much more of those earnings and able to make economic progress as they go.”

As a five-year pilot program, DHS officials are using Career MAP to examine how direct support impacts the long-term financial stability of roughly 500 actively enrolled participants.

The program is designed to serve participants who have completed the DHS Family Rehousing Stabilization Program, also known as Rapid Rehousing, which connects people with housing and rental assistance.

King says that securing housing marks a first step toward financial security. Then Career MAP aims to help participants to manage their benefits, offering guidance and financial support as they build up their annual income.

So far, King says that it looks like the program is paying off. Of the roughly 500 households participating, about 70 have increased their income enough to phase off some federal benefits and begin receiving support through the Career MAP program.

He adds that he hopes that the multi-year nature of the program helps to support participants’ needs as they arise overtime, as opposed to addressing issues on a short-term, case-by-case basis.

Sanchez’s research paper on the benefits cliff paid particular focus to the Career MAP program. He found that the program significantly alleviates the financial burden that households incur when they are cut off from public benefits. For a household earning $65,000, their annual net financial resources goes from under $10,000 without the program to more than $30,000 with Career MAP.

Sanchez adds that the program is distinct in its efforts to directly address the benefits cliff as an issue.

“They’re kind of saying head on, ‘We’re going to structure this workforce development program to actually try and mitigate these benefits cliffs,’” he says. “That’s why this program in DC is so unique.”

Ellison says that her daughter is currently enrolled in Career MAP and that the program is “a resource that was definitely needed for mothers and children and families.”

But, as a pilot program, enrollment in Career MAP was limited, and new participants are not yet being considered. Ellison says that she hopes that the program expands because securing long-term employment can be a years-long ordeal that residents are still navigating, often without enough support.

“People are scared to overcome [the benefits cliff] and find work,” she says. “It’s a process, getting the amount of courage it took for me.”

Courtesy of Street Sense Media / INSP.ngo

You may also be interested in...

Q&A: How The Big Issue Australia is empowering women through enterprise

Read more

Street Sense Media vendors stage play exploring solutions to homelessness

Read more